Featured image for this comprehensive guide about what is nvr in accounting stand for

Image source: home-cdn.reolink.us

Navigating the world of accounting acronyms can often feel like deciphering a secret code. From GAAP to IFRS, the financial landscape is dotted with abbreviations that are crucial to understanding a company’s health and operations. One such term you might encounter, especially when delving into corporate finance and equity structures, is NVR. But what exactly does NVR stand for in accounting, and why is its meaning significant for businesses, investors, and auditors alike?

Contrary to what some might initially guess, NVR in accounting typically refers to Non-Voting Rights. This concept is fundamental to understanding certain types of share ownership and corporate governance. It’s not a complex calculation or a new regulatory standard, but rather a descriptive term for a specific characteristic of a financial instrument. Let’s peel back the layers and explore the profound implications of non-voting rights in the financial realm.

📋 Table of Contents

- What Exactly Does NVR Stand For in Accounting?

- Why Do Non-Voting Rights (NVR) Exist? Strategic Business Reasons

- The Accounting and Financial Reporting Implications of NVR

- NVR and Investor Considerations: What You Need to Know

- Real-World Examples and Strategic Use of Non-Voting Rights

- Conclusion: The Enduring Significance of NVR in Accounting

What Exactly Does NVR Stand For in Accounting?

In the context of accounting and corporate finance, NVR stands for Non-Voting Rights. This designation applies primarily to shares or other equity instruments that do not grant their holders the ability to vote on company matters at shareholder meetings. Unlike common shares, which typically come with one vote per share, instruments with Non-Voting Rights offer financial ownership without directorial influence.

Understanding Non-Voting Shares

- Definition: Shares that entitle their holder to dividends and a share of assets upon liquidation but no right to vote on company policies, elect directors, or approve major corporate actions.

- Common Types: These are most frequently seen in the form of preferred shares, but some companies issue specific classes of common shares with Non-Voting Rights.

- Contrast with Voting Shares: Standard common shares typically carry voting rights, giving shareholders a say in how the company is run. NVR shares explicitly remove this power.

The distinction is critical because it separates financial interest from corporate control, an arrangement with specific strategic implications for both the issuing company and the investing shareholder.

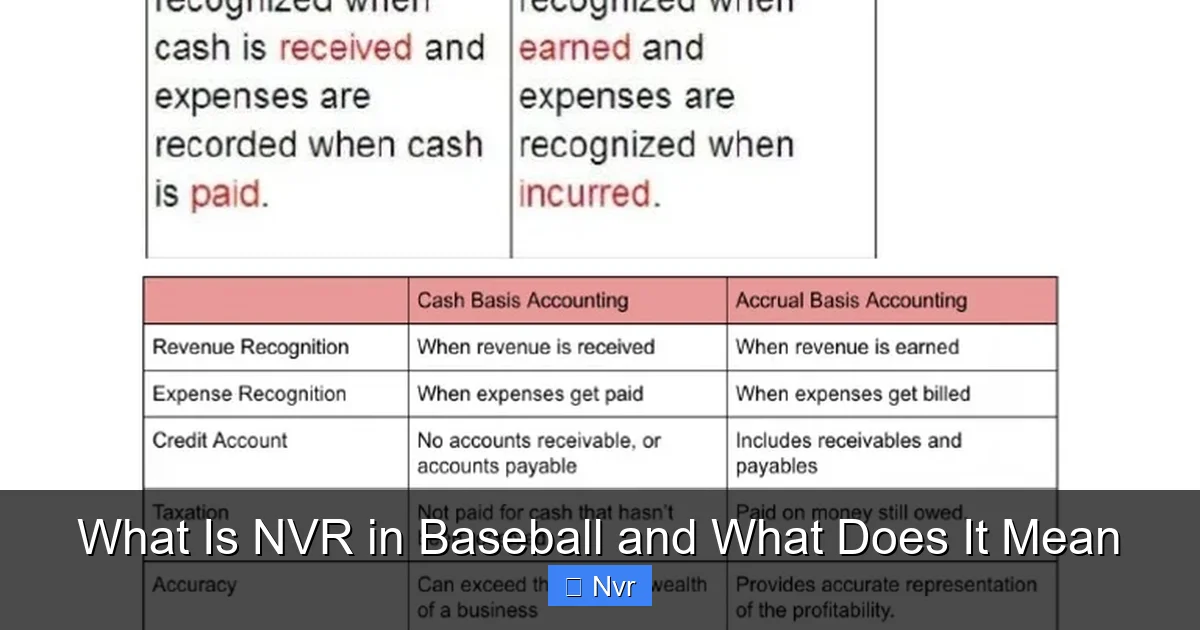

| Accounting Concept | Definition/Explanation | Key Components/Metrics | Significance/Application |

|---|---|---|---|

| NVR (Net Value Realization) | Represents the actual revenue or value received from an asset, project, or sale after deducting all direct associated costs and expenses. | Gross Revenue/Value, Direct Costs (e.g., production, selling), Operating Expenses. | Measures true profitability and efficiency; crucial for asset valuation, project viability, and pricing strategies. |

| Calculation Basis | NVR = Gross Value (or Revenue) – Direct Costs – Attributable Operating Expenses. | Example: Product Sale Price $100, COGS $30, Selling Costs $10. NVR = $100 – $30 – $10 = $60. | Provides a more realistic and actionable metric for financial analysis compared to gross figures. |

| Comparison: NVR vs. Gross Value | Gross Value reflects total income before any deductions. NVR reflects the net amount after necessary costs, showing the “realized” economic benefit. | Gross Project Revenue: $5M; Total Direct Project Costs: $2M. NVR: $3M. | NVR gives a more accurate picture for internal reporting, performance evaluation, and investor communication on a specific item or project. |

| Strategic Impact | Helps businesses understand the economic efficiency of their operations, guiding pricing, cost control, and resource allocation decisions. | Companies aim for higher NVR percentages; e.g., NVR of 70% is better than 50% for similar gross revenue. | Essential for determining fair market value, impairment testing of assets, and making informed investment choices. |

Why Do Non-Voting Rights (NVR) Exist? Strategic Business Reasons

Companies don’t issue shares with Non-Voting Rights arbitrarily. There are strategic reasons why a business might opt for such an equity structure, often balancing capital needs with control considerations. Understanding these motivations sheds light on why NVR in accounting is an important concept.

Learn more about what is nvr in accounting stand for – What Is NVR in Baseball and What Does It Mean

Image source: imgv2-1-f.scribdassets.com

Key Reasons for Issuing NVR Shares:

- Capital Raising Without Diluting Control: Founders or controlling shareholders can raise significant capital from external investors without relinquishing their decision-making power. This is particularly common in family-owned businesses or tech startups where founders wish to maintain strong oversight.

- Employee Stock Options: Sometimes, companies offer non-voting shares or share options to employees. This incentivizes employees with a stake in the company’s success without complicating corporate governance.

- Public Listing Strategies: Some companies, especially those with strong founder-led visions, might list non-voting shares on public exchanges while retaining voting control through a separate class of shares. This dual-class share structure is a common way to use Non-Voting Rights.

- Specific Investor Needs: Certain investors may prioritize dividend income or capital appreciation over voting influence, making NVR shares an attractive option if they offer favorable financial terms.

According to a study by Harvard Law School, dual-class structures (which often involve non-voting shares) have become more prevalent among newly public companies, indicating a clear trend towards founders retaining control while accessing public capital markets.

The Accounting and Financial Reporting Implications of NVR

From an accounting perspective, Non-Voting Rights primarily impact how these shares are classified and disclosed in financial statements. While the lack of voting rights doesn’t change their fundamental nature as equity, it does necessitate specific reporting practices.

Learn more about what is nvr in accounting stand for – What Is NVR in Baseball and What Does It Mean

Image source: corchacr.com

How NVR Shares Impact Financial Reporting:

- Balance Sheet Classification: Shares with Non-Voting Rights are typically classified within the equity section of the balance sheet, often under “Preferred Stock” or a specific “Class B Common Stock” designation. Their value contributes to the company’s total equity.

- Disclosure Requirements: Companies are required to clearly disclose the nature of all share classes, including those with Non-Voting Rights, in the footnotes to their financial statements. This includes details about their par value, number of shares authorized, issued, and outstanding, and any specific rights or restrictions.

- Earnings Per Share (EPS) Calculation: While NVR shares don’t confer votes, they still represent ownership. If they are common stock equivalents, they might be included in the diluted EPS calculation, impacting a key financial metric for investors.

- Corporate Governance Reporting: The existence of different share classes, particularly those with Non-Voting Rights, is a crucial aspect of a company’s corporate governance framework. This information is vital for understanding ownership concentration and control.

Accurate and transparent reporting of NVR shares is essential for stakeholders to properly assess the company’s capital structure and inherent risks and opportunities.

NVR and Investor Considerations: What You Need to Know

For investors, holding shares with Non-Voting Rights presents a distinct set of considerations. While the financial returns can be attractive, the absence of a voice in corporate decisions is a significant trade-off.

Key Considerations for Investors in NVR Shares:

- Lack of Influence: The most obvious implication is the inability to vote on critical corporate matters, such as mergers, acquisitions, executive compensation, or board elections. This means your voice cannot directly shape the company’s direction.

- Focus on Financial Returns: Investors in NVR shares typically prioritize financial performance—dividends, capital appreciation, or liquidation preferences—over direct control. They are often passive investors seeking exposure to the company’s economic success.

- Potential for Different Dividend Policies: While not universally true, some classes of NVR shares (e.g., preferred stock) may have different dividend entitlements compared to voting common shares, often with fixed or guaranteed dividend payments.

- Liquidation Preferences: Preferred shares, which often carry Non-Voting Rights, may have preference over common shareholders in the event of liquidation, meaning they get paid first after creditors.

Understanding these dynamics is crucial for investors to align their investment strategy with the type of ownership they acquire. A survey by the Investor Coalition for Fair Voting Rights indicates that over 70% of investors believe that every share should have one vote, highlighting the ongoing debate about NVR structures.

Real-World Examples and Strategic Use of Non-Voting Rights

The concept of Non-Voting Rights is not merely theoretical; it’s a practical tool used by numerous companies, from established giants to emerging startups, to manage their capital and control structure. These real-world applications underscore the importance of understanding NVR in accounting.

Companies Utilizing NVR Structures:

- Alphabet (Google): One of the most prominent examples is Alphabet, which has Class A (one vote per share), Class B (ten votes per share, held by founders), and Class C (Non-Voting Rights) shares. This structure allows founders to maintain control while raising capital.

- Meta Platforms (Facebook): Similar to Alphabet, Meta employs a dual-class share structure where founders retain significant voting power through high-vote shares, while public investors often hold shares with Non-Voting Rights or limited voting power.

- Family-Owned Businesses: Many privately held family businesses, upon seeking external investment, will issue Non-Voting Rights shares to outside investors or non-family employees to preserve family control.

These examples illustrate how NVR shares serve as a strategic instrument for maintaining control, facilitating succession planning, or structuring public offerings while attracting diverse investor pools. The flexibility offered by Non-Voting Rights can be a powerful tool in corporate finance, shaping everything from governance to growth trajectories.

Conclusion: The Enduring Significance of NVR in Accounting

In conclusion, while the acronym NVR might initially seem cryptic, its meaning in accounting – Non-Voting Rights – is a cornerstone concept in corporate finance. It defines a crucial distinction in share ownership, allowing companies to raise capital without diluting control and offering investors a pure financial stake.

From strategic capital allocation to intricate financial disclosures, understanding what NVR stands for in accounting is essential for anyone navigating the complexities of modern business. Whether you’re an entrepreneur considering your equity structure, an investor evaluating a company’s governance, or an accountant ensuring accurate reporting, recognizing Non-Voting Rights provides a deeper insight into the financial mechanics and strategic decisions that shape the corporate world. Always examine the specific rights associated with any shares you hold or issue, as the presence or absence of voting rights profoundly impacts your role and influence.

Frequently Asked Questions

What Is NVR in Baseball and What Does It Mean

What does NVR stand for in accounting?

In accounting, NVR typically stands for Net Realizable Value. This term refers to the estimated selling price of an asset in the ordinary course of business, less the estimated costs of completion and the estimated costs necessary to make the sale. It’s crucial for accurately valuing certain assets on a balance sheet.

Where is Net Realizable Value (NVR) commonly used in accounting?

NVR is most commonly used in inventory valuation, particularly under the lower of cost or net realizable value (LCNRV) rule. This principle ensures that inventory is not carried on the balance sheet at an amount higher than what the company expects to realize from its sale. It helps prevent overstating assets.

How is NVR calculated for inventory?

To calculate NVR for inventory, you start with the estimated selling price of the inventory. From this, you subtract any estimated costs to complete the inventory (if it’s work-in-progress) and all estimated costs necessary to make the sale, such as selling commissions or shipping. The resulting figure is the Net Realizable Value.

Why is NVR important for financial reporting?

NVR is important because it upholds the principle of conservatism in accounting, ensuring assets are not overstated. By valuing inventory at the lower of its cost or NVR, companies provide a more realistic picture of their financial health and protect stakeholders from misleading asset valuations. This also impacts profit calculations.

Is NVR the same as market value in accounting?

No, NVR is not exactly the same as market value, although they are related. Market value refers to the current price at which an asset could be sold in the market. NVR, however, specifically deducts future costs to sell and complete from an estimated selling price, making it a more specific, net figure pertinent to a company’s actual realization from an asset.

What accounting standards relate to NVR?

Under U.S. GAAP, NVR is directly relevant to ASC 330, Inventory, which mandates the lower of cost or net realizable value rule for inventory valuation. For companies following IFRS, IAS 2, Inventories, also requires inventory to be measured at the lower of cost and net realizable value. Both standards aim to prevent overstatement of inventory assets.